Contingencies, also called provisions, clauses, or due diligence items, are the core safeguards in place to protect a buyer’s deposit if a deal needs to be cancelled.

Contingencies are terms in a real estate contract that must be met for a sale to move forward. They protect buyers (and sellers) by allowing parties to back out of the deal—without penalty—if specific requirements aren't satisfied. Once a contract is accepted, buyers typically wire an initial deposit within a few days as a show of good faith- this is what's at risk. Common contingencies include home inspection, financing, and appraisal. These clauses give buyers time to ensure the property is what they expected it to be and that they can secure funding before fully committing to the purchase.

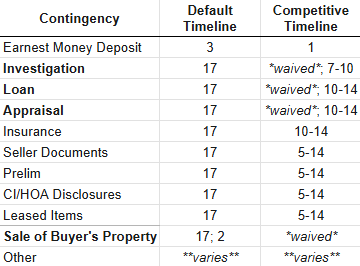

The kinds of contingencies—and how they're removed—vary by state. And within each state, the time you have to remove them can shift depending on local market conditions. In CA, the default timelines for most contingencies is 17 days, but 17 days may not be competitive enough in a seller's market. I’m including a standard (CA) list of contingencies and their default timelines at the bottom of this article.

The transaction revolves around these safeguards because of the scale of risk involved. If you’re reading this, you’re likely in a position where this hits close to home. Real estate sales aren’t just a transaction; they’re often someone's life savings, retirement plan(s), or their kids' inheritance. The money, time, and emotion at stake are often enormous.

Note: Some agents mistakenly use "conditions" when they mean contingencies. These are two different things. Conditions are documents and tasks a lender requires for final loan approval. Confusing the two causes problems, so it’s worth knowing the difference.